January 2, 2024

Echo45 Advisors Investment Committee

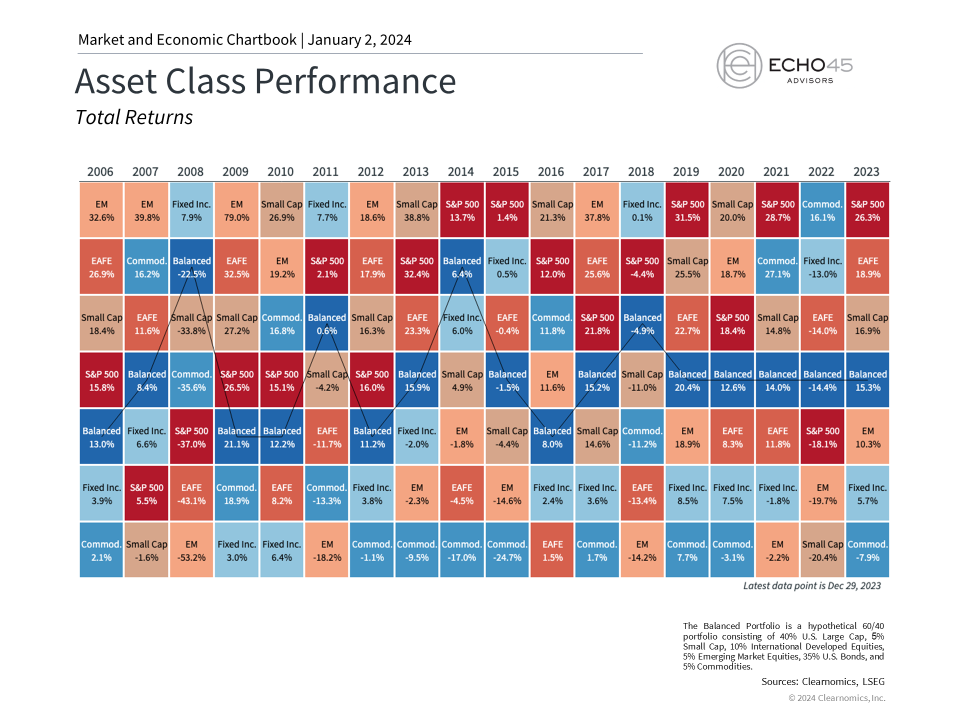

2023 marked an inflection point for markets with strong gains across both stocks and bonds. The S&P 500, Dow, and Nasdaq generated exceptional returns of 26.3%, 16.2%, and 44.7% with reinvested dividends last year, respectively. The S&P has come full circle and is now only a fraction of a percentage point below the all-time high from exactly two years ago. The U.S. 10-Year Treasury yield climbed as high as 5% in October before falling to end the year around 3.9%, pushing bond prices higher in the process. International stocks also performed well with developed markets returning 18.9% and emerging markets 10.3%. What drove these results and how could they impact investors in 2024?

Perhaps the most important lesson of 2023 for everyday investors is that news headlines and economic events don't always impact markets in obvious ways. Last year's positive returns occurred despite historic challenges including the worst banking crisis since 2008, rapid Fed rate hikes, debt ceilings and budget battles in Washington, the ongoing war in Ukraine, the conflict in the Middle East, cracks in China's economy, and many more. If you had shared these headlines with an investor at the start of 2023, they would probably have assumed there would be a worsening bear market or a deep recession.

Why isn't this what happened? At the risk of oversimplifying, the key factor driving markets the past few years has been inflation. High inflation affects all parts of the markets and economy including forcing the Fed to raise interest rates, slowing growth, hurting corporate profits, dampening consumer spending, and acting as a drag on bond returns. This is exactly what occurred in 2022 but many of these effects reversed in 2023 as inflation rates improved.

The headline Consumer Price Index, for instance, jumped 9.1% in June 2022 on a year-over-year basis but only grew 3.1% this past November. Unfortunately for consumers and retirees, this does not mean that prices will fall back to pre-pandemic levels - only that they will rise more slowly. For markets, however, what matters is that the rate of change is slowing and that core inflation could gradually approach the Fed's 2% long run target.

Thus, the recession that was anticipated by markets a year ago has not yet occurred. While many still expect economic growth to slow this year, it's not unreasonable to suggest that the Fed could achieve a "soft landing" in which inflation stabilizes without causing a recession. This is why both markets and Fed forecasts show that they could begin to cut policy rates by the middle of the year.

What does this mean for the year ahead? If 2022 was characterized by the worst inflation shock in 40 years, leading to a bear market in stocks and bonds, 2023 saw many of these factors turn around. These trends could continue if the Fed does begin to ease monetary policy. Of course, much is still uncertain and investors should always expect the unexpected when it comes to market, economic, and geopolitical events. After all, markets never move up in a straight line and even the best years experience several short-term pullbacks.

The past year has shown us that it's important to stay invested and diversified across all phases of the market cycle, rather than try to predict exactly what might happen on a daily, weekly, or monthly basis. Below are five key insights into the current market environment that will likely be important in 2024.

1. Many asset classes performed exceptionally well in 2023

Strong economic growth and falling rates propelled many asset classes higher last year. Stocks reversed much of their losses from the previous year with a historically strong gain and bonds bounced back as interest rates fell in the final months of the year. Technology stocks, especially those related to artificial intelligence, helped to drive market returns as well, pushing the Nasdaq to a nearly 45% return. While the so-called "Magnificent 7" did double in value, other sectors also began to perform better as market conditions improved.

Most importantly, there are signs that earnings growth is recovering. Earnings-per-share for the S&P 500 are expected to have been flat in 2023, but Wall Street consensus estimates suggest that they could grow by double digits each of the next two years. While this will depend on the path of economic growth, any increase in earnings will help to improve valuations and support the stock market.

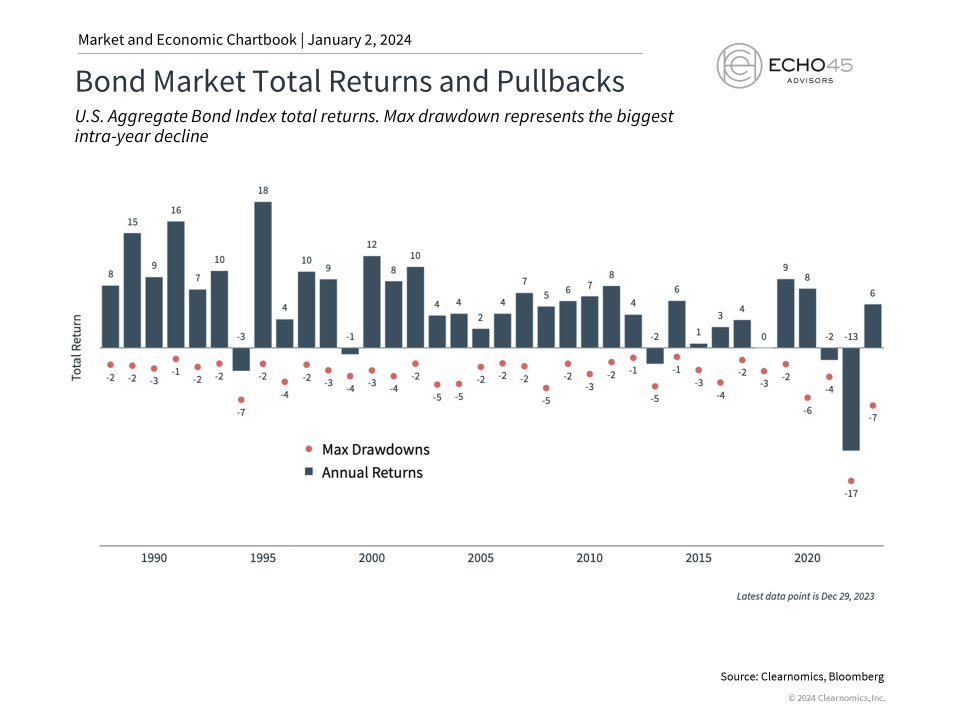

2. Bonds have rebounded as interest rates have stabilized

Bonds had a much better year with interest rates rising through October then falling on positive inflation data. While bonds have not recovered their 2022 losses after a historic spike in inflation, recent performance shows that bonds are still an important asset classes that can help to balance stocks in diversified portfolios. This is true across many sectors including high yield, investment grade, government bonds, and more.

3. The Fed is expected to cut rates in 2024

Improving inflation coupled with a historically strong job market have helped the Fed to achieve its policy objectives. While it's too early to declare victory, many expect the Fed to begin cutting rates in 2024. The Fed's own projections suggest they could lower rates by 75 basis points by the end of the year. Market-based expectations are much more aggressive and are expecting twice as many cuts. While it's hard to predict exactly what the Fed may do this year, the fact that rates could begin to fall could help to support financial markets and the economy.

4. The economy has been remarkably strong

The economy has been stronger than many expected over the past twelve months. GDP grew by 4.9% in the third quarter, one of the fastest rates in recent years. Consumer spending helped as did a rebound in business investment as the interest rate outlook stabilized. Unemployment is still only 3.7% and while monthly job gains have slowed somewhat, the labor market is still far stronger than economic theory would have predicted given the sharp increase in interest rates.

5. The most important lesson for investors is to stay invested

While the past twelve months have been positive for investment portfolios, investors should not become complacent. Volatility in the stock market is both normal and expected with even the best years experiencing short-term swings, as shown in the accompanying chart. Rather than trying to predict exactly when these pullbacks will occur, it's more important for investors to hold diversified portfolios that can withstand unforeseen events. The past few years are a reminder that holding an appropriate portfolio is the best way for investors to achieve their long-term financial goals.

Echo45 Advisors LLC is a Registered Investment Advisor. The information and statistics in this report has been obtained from Clearnomics, a separate and unaffiliated organization. Based on our own due diligence, we believe Clearnomics to be reliable but we do not warrant their accuracy or completeness. This report is for your information only and does not constitute an offer to buy or sell, or the solicitation of any offer to buy or sell any securities. Advisory services are only offered to clients or prospective clients where Echo45 Advisors LLC and its representatives are properly licensed or exempt from licensure. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by Echo45 Advisors LLC unless a client service agreement is in place.

Copyright (c) 2024 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company’s stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security--including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.